Key Takeaways

1. UK government ‘IR35’ rules around off-payroll working by contractors in the private sector changed in April 2021.

2. IR35 rules are designed to combat PAYE tax avoidance through ‘disguised employment,’ a practice whereby employees are incorrectly classified as contractors, allowing clients and contractors to pay less tax and National Insurance Contributions.

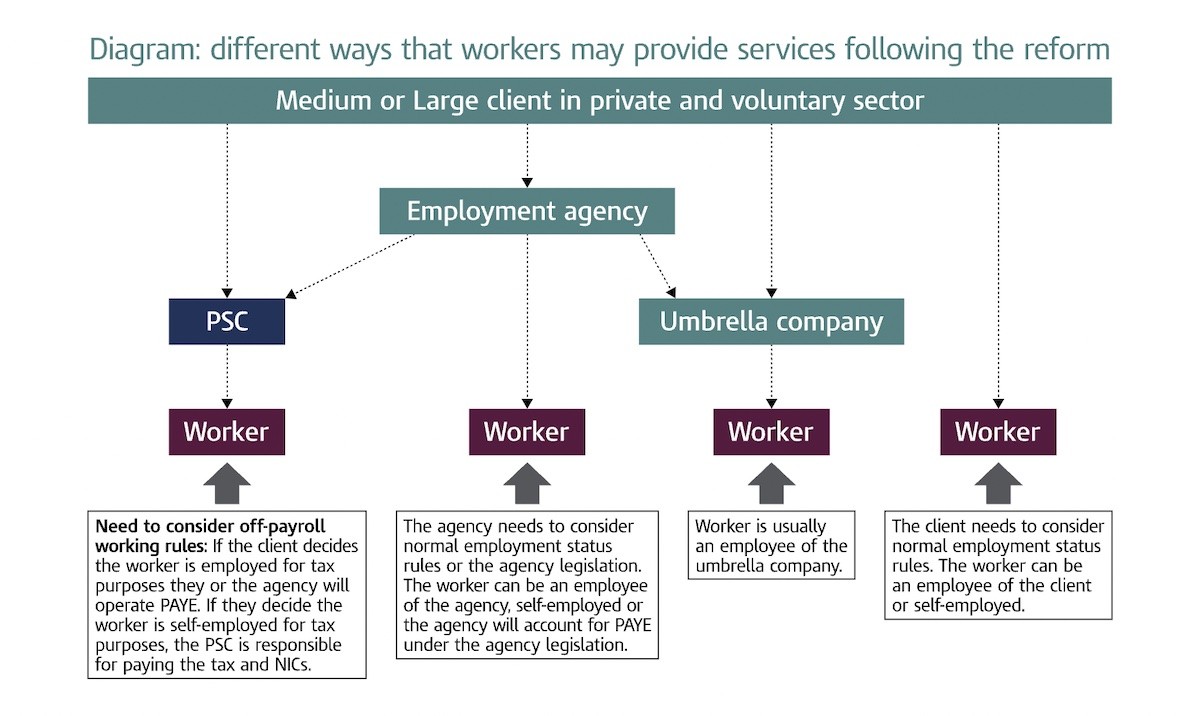

3. Medium to large end clients are now responsible for correctly classifying contracts according to IR35 criteria. Workers and agencies involved in the employment chain must also ensure that each contract’s IR35 status is correct. Small businesses are exempt.

4. Her Majesty’s Revenue and Customs (HMRC) applies specific criteria to distinguish self-employed contractors from regular employees. There are also some legal grey areas. Contractors and the companies who hire them may benefit from taking expert advice before agreeing on assignments to maintain legal compliance and tax-efficient operation.

Since April 2021, end-users have been responsible for evaluating the IR35 status of contractor assignments. If the assessment shows that contractors are ‘deemed employees’ for HMRC purposes, the end-client must pay relevant tax, National Insurance, and Health and Social Care contributions.

Whether you’re a contractor with your limited company or a business leader wondering how IR35 rule changes might affect your contingent workforce and bottom line, our article explains the key facts and context you need around off-payroll working in the UK today.

What is IR35?

IR35 is the common term that describes the application of rules around UK off-payroll working under legislation designed to combat tax avoidance. The term came from the Inland Revenue press release announcing a government clampdown on disguised employment in 2000 (this is similar to the notion of ‘employee misclassification‘ in other countries such as the US). IR35 rules target contractors who are considered to be ‘disguised employees’ according to HMRC criteria.

Two relevant areas of law govern IR35:

- Section 8 of the Income Tax (Earnings and Pensions) Act 2000

- The Social Security Contributions (Intermediaries) Regulations 2000

Video: How IR35 Works

How are contractors taxed in the UK?

Employees and contractors are treated differently under UK employment law and tax laws.

Suppose a contractor provides services through their limited company without receiving employee benefits (pension contributions, sick pay, annual leave allowance, etc..). In that case, they will generally be taxed differently than employees.

Contractors may take some of their pay in dividends from their company instead of taxable salary. They can also offset many business expenses against tax and will pay less in National Insurance Contributions.

The lower tax requirements reflect the greater financial risk of being self-employed.

Aside from limited companies, the self-employed might also choose to operate as a sole proprietor or sole trader, though, in that case, they will pay taxes on their income at full personal income tax rates (not corporate rates).

It should also be observed that contractors in the UK are often eligible for the tax-free trading allowance that does not apply to employee income.

How did IR35 change in 2021?

New off-payroll rules were introduced in the UK in April 2021. These changes brought those working for medium to large private sector firms into line with amendments already implemented across the public sector in April 2017.

Under updated IR35 rules, contractors operating through limited companies in the private sector can no longer independently set the IR35 status of their assignment. Responsibility for selecting the correct IR35 status lies with the end client (except for exempt small businesses). The contractor, client, and any intermediary parties involved must ensure they remain IR35 compliant.

After making an IR35 status assessment on a contract, the end client must pass a record of this evaluation – including the decision, reasoning, and evidence of “reasonable care” – to all relevant parties. This document is known as a Status Determination Statement (SDS). If the contract is amended, the client must create a new SDS, assessing whether changes have altered the IR35 status of the relationship with the contractor.

If the contractor disagrees with an SDS decision, they can appeal within 45 days, and their client will have an additional 45 days to consider and respond to their appeal. If a client company doesn’t meet the 45-day limit for response, they become liable for taxes and NICs incurred by the contractor due to changed IR35 status.

Who does IR35 apply to?

IR35 rules must be checked by:

- Workers who provide services through an intermediary entity (limited company, partnership, etc..)

- Clients who receive services from a worker via a limited company or other intermediaries.

- Recruitment and other agencies providing workers’ services.

Contractors will be ‘caught’ by IR35 rules when they provide services to their clients via an intermediary legal entity and if they would be classified as employees without using the intermediary entity.

HMRC uses specific criteria to determine whether contractors lie ‘inside’ or ‘outside’ IR35. Some requirements are common sense and will show quickly and clearly that certain workers are contractors or employees. If unsure, an HMRC online tool allows you to make an unofficial employment status check.

Stricter IR35 rules have nudged some limited company contractors into moving to an ‘umbrella’ working model where they become temporary employees of an umbrella company. Umbrella company workers pay the same tax as ‘inside’ IR35 contractors but receive benefits, including holiday and sick pay entitlements. Umbrella working is typically temporary and does not provide the same long-term employment solutions as a Global PEO service.

There are several legal grey areas where contractors and client companies might benefit from professional advice before agreeing or renewing a contract to ensure they remain compliant and tax-efficient.

What happens if a non-employee worker meets IR35 criteria?

Tax and National Insurance payments

HMRC classifies workers falling inside IR35 as ‘deemed employees’. On this basis, the end client (or recruitment agency, if involved) must pay income tax and employers’ and employees’ National Insurance Contributions (NICs) for these contractors, just as for any other ordinary employees in the same tax bracket. This can potentially reduce a contractor’s net income by 25%.

Employment rights and benefits

If contractors are caught inside IR35 and are liable to pay taxes as employees, this does not automatically confer full employment status beyond tax obligations. IR35 employees are not entitled to employment rights and benefits such as pension contributions or annual leave.

Penalties

Penalties may be given by HMRC if a contractor now caught by updated IR35 rules was found to have been previously classified outside IR35 and, therefore, paid less tax than they should have done in earlier tax years. These contractors and their end-clients must pay missing taxes plus interest and penalties back. HMRC has powers to investigate up to six previous tax years.

While the UK government has stated that it does not plan to enforce penalties for accidental rule-breaking by those who have taken “reasonable care,” they have also been clear in plans to punish and publicly identify companies who deliberately break the rules.

Evidence of “reasonable care might include gathering and recording information on whether the contractor has other clients, whether their work entails financial risk, and working patterns and practices which are not identical to those of employees.

When does HMRC consider a contractor to be a 'deemed employee'?

HMRC can conduct IR35 compliance checks on contractors, investigating the wording of contracts and working practices while delivering contracts. The outcome of an HMRC check would determine whether a contractor should be considered employed or self-employed for tax purposes.

Factors considered as part of HMRC’s decision-making on whether a contractor lies inside or outside IR35 include:

Mutuality of obligation

Suppose a contract contains clauses obligating a client to give further work or for a contractor to accept other work. In that case, this implies mutuality of obligation, a key characteristic of an employment relationship rather than self-employment. Contracts set to roll over or continuously renewed could also imply mutuality of obligation and place the contract within IR35 rules.

Right of substitution

Another key characteristic of an employment relationship is having one individual assigned to carry out a particular role. Where this constraint is built into a contract, the worker is more likely to be considered within IR35. Suppose a contractor is free to carry out contracted duties themselves or hire someone appropriate to complete them. In that case, they are more likely to be considered self-employed and outside IR35.

Right of control

Generally, the more control exerted over a contractor by a client, the more likely the assignment falls within IR35 rules. Contracts that specify work in detail, including when, where, and how it needs to be completed, strongly imply an employment relationship and are likely to fall within IR35.

Shifting contractors to meet client business priorities or controlling contractor workstreams and performance through a corporate line-management system are examples of contexts likely to be found in employment situations.

If contractors have autonomy in delivering their contractual obligations, this is more indicative of self-employment falling outside IR35.

What other factors contribute to HMRC’s decision?

IR35 regulations are complex, and HMRC may consider and balance a wide range of information on individual cases, including contract wording, context, and working practices. Contracts resembling those of comparable full-time employees will likely be caught inside IR35. Relevant considerations can include:

Employee benefits

Workers receiving learning and development courses, annual leave, sick pay, and pension contributions are likely to be considered as employees. These benefits are not normally given to contractors.

Financial outlay for work

Contractors may have to pay for their equipment, training, software, etc., while employees normally have everything they need to work provided by their employer.

Termination of contract

Employees normally have a set notice period agreed upon in their contract. Clients can terminate the assignment of a contractor immediately and without notice.

Horizons and IR35 Compliance

Despite IR35 changes and ongoing challenges and risks around Brexit, the UK offers growth opportunities and an impressive talent pool for many businesses. Companies operating in the UK must ensure they understand and are able to comply with the updated IR35 regime. Horizons offer Global PEO solutions in the UK as part of their international work across 180+ countries. Get in touch today for tailored guidance on IR35 and wider UK business needs.

Frequently Asked Questions

IR35 rules are intended to combat tax avoidance by contractors who are effectively operating as employees while benefiting from the self-employed tax regime. Contractors who fall clearly outside IR35 are deemed self-employed by HMRC and are able to pay lower overall levels of tax and National Insurance Contributions. IR35 contractors who fall within the HMRC off-payroll rules must pay tax and national insurance on the same basis as any other employee performing their role.

Contractors who are fully and clearly self-employed according to HMRC criteria will be considered outside IR35.

In terms of end-clients, small businesses (as defined in the Companies Act 2006) are exempt from IR35. Companies are always considered as ‘small businesses” in their first financial year of trading. After that, they will be considered small if two of the following criteria are met over two consecutive financial years:

– Annual turnover £10.2 million or less

– Balance sheet total of £5.1 million or less

– No more than 50 employees for the company’s financial year.